Gulf-Maghreb Relations: Investing without Interfering

Eckart Woertz

Senior Research Fellow Associate, (CIDOB)

22 May 2013 / Opinión CIDOB, n.º 190 / E-ISSN 2014-0843

The Gulf and Maghreb countries share a common heritage and are members of the Arab League, yet the record of their economic and political relations is mixed. Limited exchange in physical goods is juxtaposed with pronounced investment activities in tourism and real estate that are at times controversial. Openness to Gulf investments is accompanied by growing reservations about Gulf support of Islamist forces in the region, most notably by Qatar.

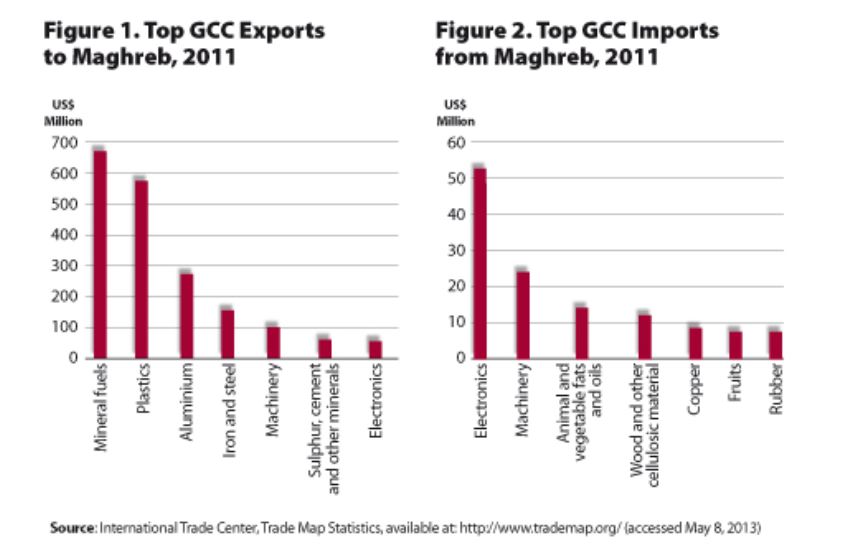

Trade between the two regions is small compared with other regions. Maghreb countries only contributed $174 million to $370 billion of imports into the GCC countries in 2011, and absorbed $2.3 billion worth of exports from there, which was insignificant given the total GCC exports of $784 billion. GCC exports mainly consisted of oil, plastics, and other products of their heavy industries like aluminum and steel, and also sulphur, which Morocco imports in large quantities for its phosphate fertilizer industry. Maghreb countries in turn mainly exported electronics, machinery and agricultural products to the GCC (see Figures 1 and 2).

The trade profiles reflect the limited complementarity of economies that have a strong focus on production of raw materials, despite considerable investments in diversification. This is true not only for the oil exporters in the Gulf, Libya and Algeria, but also for Mauritania with its iron ore mines and Morocco, which is the largest phosphate exporter worldwide and commands about three quarters of global reserves after a massive upgrade of resource estimates by the US Geological Survey in 2011. The political compartmentalization of the Maghreb and the lack of intra-regional cross-border trade is another hindrance.

Geography also impedes enhanced exchange. Morocco is 20 kilometers away from Spain, but over 5,000 from the Arabian Peninsula. Naturally, Mediterranean countries like Italy, Spain and France are among the most important trade partners of the Maghreb countries. The Greater Arab Free Trade Area (GAFTA) does not have the same allure and effectiveness as association agreements with the European Union that the Maghreb countries signed in the 1990s. They might lead to more comprehensive free trade agreements (FTAs) in the future. Morocco was the first country in Africa to sign such an FTA with the US in 2004. In comparison, its interest was lukewarm in the GCC membership that it was offered recently. With its large coastline, Morocco is also keen on intensifying trade with Latin American countries of the southern Atlantic area, most notably the agricultural powerhouses like Brazil and Argentina, which are customers of its fertilizer products. Maghreb countries also intend to expand trade relations with West Africa for reasons of geographical proximity. The Gulf countries, on the other hand, export over two thirds of their oil to Asian countries. Thus, when it comes to trade, the Gulf and the Maghreb look in opposite directions.

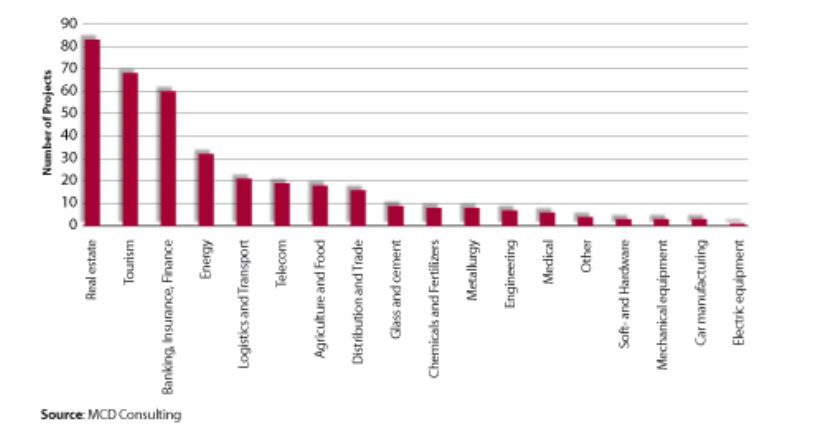

If physical goods trade is limited, the picture changes when it comes to investments. Gulf investments in the 2000s focused on real estate and tourism, followed by banking (see Figure 3). Morocco, in particular, is a popular travel destination among Gulf nationals. Its tourism sector contributes 10 per cent to the GDP, with an annual growth rate of 12 per cent over the last decade. In May 2013, several Gulf leaders, including Sheikh Hamad bin Khalifa Al-Thani, the Amir of Qatar, and Shaikh Mohamed bin Zayed Al Nahyan, the Crown Prince of Abu Dhabi, signed a partnership agreement with Morocco that included the establishment of a Tourism Investment Authority. The UAE and Saudi Arabia have invested in wind and solar energy projects in Morocco as all three countries aim to add renewables to their energy mix. Qatar has announced investments in Tunisia’s phosphate industry and an Algerian steel mill. It has also tried to get a foothold in the natural gas industry of Libya in the wake of the fall of the Gaddafi regime.

Figure 3: Sectoral Distribution of Gulf FDI in the Maghreb (2003-2011)

The Gulf countries now contribute a large share of foreign direct investments (FDI) in the Maghreb. Accounting for about a fifth of Moroccan inward FDI, they come right after France and other European countries, for example. Yet it is not all smooth sailing. The Gulf countries have a reputation for focusing on capital-intensive projects, short-term profitability, and acquisition of non-duplicable infrastructure in order to access quasi-rents (e.g., in the telecom and transport sectors). In contrast to other countries, their investments lead to fewer joint ventures and less crucial know-how transfer. Like at home, Gulf real estate investments target the upscale luxury market and can crowd out domestic communities and businesses.

Resentments are exacerbated by the increased political profile of Gulf countries in the region, which is at times perceived as meddling in domestic affairs. Qatar’s support for the Islamist Ghannouchi government in Tunisia and the financing of Salafist groups by Saudi and other Gulf nationals have caused concern. Austere interpretations of Islam meet with skepticism in the Maghreb, which has a rich tradition of mystic Sufism and a history of secular modernization. The attempt of the Ghannouchi government to water down women’s rights in the draft for a new constitution has met with fierce resistance. Similarly, the destruction of Sufi shrines and the murder of opposition leader Chokri Belaid by Salafist groups with alleged ties to Ghannouchi’s Ennahada party led to a national outcry in February 2013. The UGTT trade union federation threatened a general strike and Ghannouchi was forced to reshuffle his cabinet.

In sum, there is a strong case for increased economic cooperation between the Gulf and the Maghreb that goes beyond coordination of oil production quotas by the OPEC members in both regions. Gulf capital and skilled labor in the Maghreb have the potential for synergetic relationships, especially if a more broad-based approach is chosen that goes beyond an excessive focus on luxury real estate. However, any engagement should respect local traditions and should be strictly based on the principle of non-interference in domestic affairs.

(*) A former version of this opinion piece was published by the Gulf Research Center, Geneva;