Spain and the Maghreb: neighbourhood, nearshoring and the post-pandemic

This article is an updated version of a working document inspired by the foreign policy dialogues organised by CIDOB and CITPAX with the support of the State Secretariat for Global Spain of the Ministry of Foreign Affairs, European Union and Cooperation, which took place on February 19th 2021 under the title "Nearshoring in the Maghreb: priorities and impact on Spain".

Can geographical proximity, so often an irritant, begin to generate mutual opportunities? This is the possibility that has opened up for Spain and its Maghrebi neighbours with the global discussion on the need to shorten supply chains. It is both an economic and geopolitical undertaking. The bilateral crisis that broke out between Morocco and Spain in May 2021 increased the importance of this issue, as it highlighted both the strategy’s weaknesses and the urgent need to generate positive agendas. But opportunities can also be missed. Whether it succeeds or not will depend on what a range of actors do – or stop doing – in Spain, in the EU and above all in the Maghreb countries.

Spanish policy towards the Maghreb: conceptual architecture

The importance of the Maghreb and, more broadly, the Mediterranean neighbourhood is one of the few Spanish foreign policy issues that is not up for debate. The relationship is the product of a history of intense but not always easy ties. Above all, though, it has been determined by geographical proximity – by the 14 km Strait of Gibraltar, the physical borders with the autonomous cities of Ceuta and Melilla, the 500 km between Barcelona and Algiers (the same distance as between the Catalan capital and Madrid), the 300 km separating Oran from Alicante and the 560 km between the northern shores of Tunisia and the Balearic Islands. Over on the Atlantic side, barely 100 km separate the Canary Islands from southern Morocco and widening the focus we see the 800 km sea crossing between Mauritania and Tenerife. Paris may appear to be a nearby capital to Madrid, but both Rabat and Algiers are closer. So, there is no disputing whether the Maghreb matters to Spanish foreign policy, the only doubts surround what form these relations should take, who the priority partners are and what instruments can help achieve its objectives.

One of the most successful conceptualisations of Spanish policy towards the Maghreb is the “colchón de intereses” (mattress of interests). Coined in the 1980s and subsequently adopted by executives of different political hues, it can be summed up as the drive to strengthen trade and investment between Spain and its southern neighbours in order to reduce the risk of bilateral tensions. Such bonds of interdependence, the idea goes, build a “mattress” that acts as a buffer against crises, because they increase the costs to both parties of exploring the path of confrontation.

The “colchón de intereses” was designed primarily for Morocco, the country with the most latent sovereignty disputes with Spain and a convulsive shared history. In 1991, this desire to deepen and diversify bilateral relations was set down in black and with the signing of the Treaty of Friendship, Good-Neighbourliness and Cooperation. The model later served as a reference for the treaties signed with Tunisia (1995), Algeria (2002) and Mauritania (2008).

Along with the “colchón de intereses”, the other pillar of Spanish policy is Europeanisation. Spain believes it can better defend its interests beneath the European umbrella than by acting unilaterally. Hence, the repeated insistence that its relations with its Maghrebi neighbours, good or bad, are of unavoidably European significance. Three issues stand out in this process of what the literature has called “bottom-up Europeanisation” regarding the Spanish sovereignty over Ceuta and Melilla, the control of migration in the Mediterranean and the Atlantic as well as the fisheries agreements.

Spain has not only transferred problems to the European agenda, but solutions too. Spanish diplomats and society have played an active and constructive role in promoting Mediterranean initiatives. This activism culminated in the 1995 creation of the Euro-Mediterranean Partnership, also known as the Barcelona Process, and Spain has continued to be one of the main supporters of the Union for the Mediterranean (UfM). Along with these regional cooperation frameworks, Spain has encouraged the strengthening of bilateral relations between the EU and its neighbours in the Maghreb by promoting new fields of cooperation, making existing association agreements more sophisticated and providing them with greater resources.

Changing the mattress

The principles behind the “colchón de intereses” and Europeanisation remain valid, but the context created by the pandemic and the bilateral crisis with Morocco have accelerated the need to modify them. To stick with the metaphor, it is said that no matter how good a mattress is, it must be turned regularly and changed every ten years. At a time of global change accelerated by COVID-19, the cooperation agenda between Spain and the Maghreb countries could also do with freshening up. This coincides with a European-level process of agenda renewal in trade and neighbourhood policy and with a review of Spain’s Foreign Action Strategy.

At the intersection of these strategic renewal processes an increasingly prominent idea is nearshoring. This variant of reshoring consists of bringing previously relocated production to a territory closer to home. Why? Relocation to neighbouring countries allows transport times to be cut (along with economic and environmental costs) and reduces the risk of supply disruptions.

At the height of the pandemic, European economies suffered due to their dependence for the supply of essential goods on the large Asian economies, especially China. Nearshoringis proposed as a strategy that can help reduce these dependencies and increase the EU’s strategic autonomy.

The Spanish government’s Foreign Action Strategy 2021–2024 clearly reflects this idea: “Spanish foreign action will analyse the opportunities presented by the new configuration of global value chains and the redefinition of the European Union's trade and industrial policy” (p.55). The strategy document goes on to insist that Spain has "the opportunity to expand its presence in the Southern Neighborhood, becoming a hub for investment and trade with this region" (p.55).

The Communication from the European Commission on the trade policy review published in February 2021 makes a similar diagnosis: “The combination of an exponential increase in demand of certain health related critical products with supply shortages due to lock-down or restrictive measures has exposed some vulnerabilities in the health sector” (p.7). Among the solutions it presents are the diversification of production and supply chains and the promotion of production and investment in neighbouring countries and Africa.

The UfM and the OECD have also produced a report that identifies the opportunity in this area, while taking an even broader perspective in terms of regional integration. Meanwhile, a study by the Center for Mediterranean Integration, an organisation supported by a number of states, the World Bank and other international organisations, also emphasises the need to encourage further integration of Mediterranean economies in global value chains.

So nearshoring, as a concept, is on the table, just as the “colchón de intereses” was before. But are the two compatible? Does nearshoring have enough traction to freshen up the old mattress of Spanish foreign policy and give it greater buffering capacity? Could it be a way to build closer and more cooperative neighbourhood relationships? What part of this strategy can be developed in foreign policy terms and what should be integrated into the EU's external action?

What’s changed?

The process of updating Spanish policy towards the Maghreb should reflect the changes taking place at various levels. At global level, for example, a sense of vulnerability in the supply of strategic products has grown significantly. As we have seen, this factor has been interpreted as an opportunity for investment in the Maghreb countries. This sense of vulnerability began with the pandemic and the bottlenecks in healthcare supplies and was reinforced by overlapping with two other crises: the blockage of the Suez Canal in March 2021 and the shortage of semiconductors – mostly produced in Taiwan – that paralysed the car industry, among others.

A second change is the renewed pull of geopolitical thinking, understood above all in terms of the competition between great powers. This was accelerated by COVID-19, as vaccines became tools for consolidating or increasing influence, with China and Russia making the most obvious use of vaccine geopolitics. The Maghreb is no exception. Morocco quickly sought to secure the Chinese vaccine and negotiated the purchase of AstraZeneca doses produced in India. Algeria tried to take advantage of its good relations with Moscow by announcing a preliminary agreement to manufacture Sputnik V on Algerian territory from September 2021. Tunisia also received an initial delivery of the Sputnik vaccine in March 2021.

But as well as global competition, multilateral cooperation has also emerged, with COVAX the best-known mechanism. In March 2021, the multilateral initiative, which seeks to deliver vaccines to all countries regardless of their income level, made its first shipment of Pfizer vaccines to Tunisia. Attempts have also been made to build solidarity mechanisms at regional level, with varying degrees of success. Despite a number of failures and the usual recurring tensions, the European Union has gone furthest, both in terms of its strategy of a shared fight against the pandemic and in economic reconstruction and solidarity planning for its members. While the EU has set up aid mechanisms for third countries as part of the Team Europe initiative, the deteriorating health situation due to the spread of the Delta variant – especially in Tunisia – has led to criticism on Maghrebi social networks about the scant support received from European neighbours.

The African Union deserves credit for being one of the first organisations to establish a regional strategy, giving an active role to its Africa Centres for Disease Control and Prevention (Africa CDC) and negotiating a joint purchase agreement with Johnson & Johnson. The Maghreb countries participate in this collaborative African effort, but there has been no Maghreb-level coordination to tackle the pandemic. At most, specific aid has been sent between neighbouring countries, especially from Algeria to Tunisia. Once again, the Maghreb stands out for its lack of trust and low levels of dialogue and cooperation when compared with other regions of the world, which not even a global pandemic breaking out has been able to heal.

In fact, intra-Maghrebi relations have actually worsened since COVID-19 reached the region. Deteriorating relations between Algeria and Morocco are one example. Another is the thawing of the previously frozen conflict in the Sahara. In November 2020, following weeks of increased hostilities in the Guerguerat area, the Polisario Front announced the end of the ceasefire. This coincided with a very intense diplomatic campaign by Morocco to get friendly countries to recognise its sovereignty over the territory of the former Spanish colony. Right at the end of his presidency, Donald Trump brought the most significant change. In a series of tweets, the then US president announced the recognition of Moroccan sovereignty over the Sahara and the normalisation of relations between Morocco and Israel. Months later, this support for the Moroccan position would trigger diplomatic crises with Germany and Spain.

The counterpoint to the escalating tension is Libya, with a ceasefire announced in Geneva in October 2020 followed by a political agreement to launch a transitional government in February 2021. This is good news for the entire region and Spain has been supportive of the process, with Prime Minister Pedro Sánchez visiting Tripoli in June and the Spanish embassy reopening in the Libyan capital.

Beyond the uneven progress of these two conflicts, both of which have regional implications, the other element of concern is the risk of social implosion. 2021 marks the 10th anniversary of the Arab Spring and the year began with protests on the streets of Tunisia, the country where the fuse was first lit and whose still-unconsolidated democratic transition has failed to satisfy its people’s longing for social justice. Meanwhile, in Algeria the Hirak protests resumed after several months of pandemic-related lockdown. Morocco has also witnessed demonstrations against the deteriorating socio-economic situation, albeit in a more localised way. Across the region, COVID-19 has amplified the problems of unemployment, informal employment and inequality, while in places such as Tunisia vaccination management and the pressure on public healthcare also fuel social unrest and discontent with the political class.

The changes underway in European politics also condition Spanish policy towards the Maghreb. Some of these trends predate the pandemic, but have been accelerated by it. One is the ecological transition, where the European Green Deal and emission-reduction pledges are the main reference points. Another is the desire to catch up in the digitalisation race. We might also add the desire to improve the European Union’s geopolitical reflexes and to endow itself with greater strategic autonomy. These overriding priorities have permeated the vast majority of strategies, policies and cooperation frameworks promoted by the EU and are also clearly visible in the new Agenda for the Mediterranean proposed in a joint communication by the European Commission and the High Representative in February 2021.

This EU transformation programme could have uneven effects: it presents an opportunity for those able to take advantage, but a potential risk for those left out. The green transition and the promotion of decarbonisation strategies clearly exemplify this. Countries like Morocco – well-placed in the field of renewable energies and the development of green hydrogen – may benefit, but for hydrocarbon-producing countries like Algeria the policies pose a major challenge.

Then there is the EU’s rising interest in Africa as a whole. If the Maghreb countries manage to position themselves as connectors, it presents an opportunity. But there is a risk that Europe’s renewed commitment to Africa will be to the detriment of its closest neighbours. The same is true of nearshoring, one of the ways identified to achieve strategic autonomy. It could give the Maghreb countries (and Spain) an opportunity, but they are not the only ones looking to take advantage of this realignment. Turkey, Egypt and eastern European countries will also put themselves forward, and here the Maghreb countries’ lack of mutual cooperation works against them, as it reduces the size and attractiveness of their market.

The changes taking place within Spain are also worth noting. The country has been among Europe’s hardest-hit by the health crisis and its economic repercussions, not least because of the importance of tourism and business trips to the Spanish economy, particularly in the coastal regions. As well as economic there are political challenges: fragmentation and political polarisation increase the likelihood of the Maghreb (and relations with Morocco in particular) becoming a political weapon at national, regional and even local level.

Morocco, Algeria and Tunisia: three very different partners

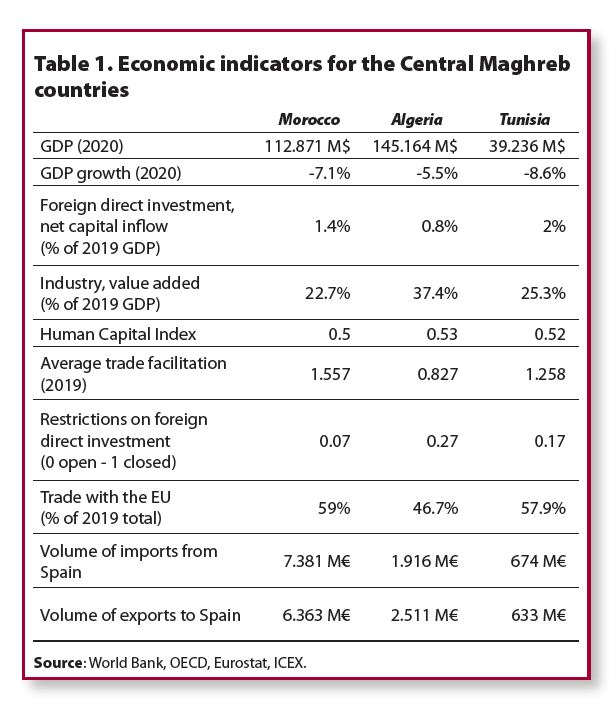

In a recent article on the possibilities nearshoring offers the Maghreb and the European Union, Francis Ghilès underlined the differences between the three central Maghreb countries. In his analysis, Morocco begins with an advantage thanks to the modernisation and dynamism of its productive fabric and its investments in infrastructure. Algeria is a clear case of wasted potential (especially given the size of its market), due to a lack of openness to international investment that, among other things, weakens the competitiveness of its once powerful industrial sector. Tunisia could take advantage of its skilled workers, its export-focussed industrial structure and the international will to support the consolidation of its democratic transition, but these three strengths are undermined by poor administrative management, lack of reforms and political uncertainty.

As the table above shows, the three central Maghreb countries begin from very different starting points. Nevertheless, any initiative to promote nearshoring processes to bring industrial production closer to neighbouring countries and further integrate them into global value chains aligns with Spanish and European interests. For key sectors such as the automotive and pharmaceutical industries, the benefit would materialise in increased security of supply and reduced transport costs. In principle, these are the same priorities set by the Maghreb countries themselves. For example, in June 2020, in order to achieve the target of securing supplies while diversifying the economy, Lotfi Benbahmed, Algeria’s Minister of the Pharmaceutical Industry, announced that the country hoped to cover 70% of its drug needs locally by mid-2022. Implementing these plans, not only in Algeria but also in Morocco and Tunisia, will require infrastructure, training (insufficient according the World Bank’s Human Capital Index) and reducing investment barriers where they are highest.

This strategy would contribute to the region’s economic progress by creating jobs, generating opportunities and increasing disposable income. It would also have a direct impact on Spain. One figure illustrates this better than a thousand speeches: in 2019, before the pandemic, Spain exported more to Morocco (€8.45 million) than to China (€6.80 million). Clearly, a key client increasing its purchasing power and industrial demand should have a positive effect on the Spanish economy. Over 600 Spanish companies have bases in Morocco and a successful relationship of industrial complementarity has developed in the Strait of Gibraltar, which partly explains the increased trade flows between the two countries. In other words, relatively solid foundations to build on are already in place.

One of the main obstacles in the way of a firm commitment to nearshoring are Morocco’s irritable political relations with both Spain and the EU as a whole. The Sahara issue has always been there, but it has gained prominence and has the potential to create further distortions. The crisis between Spain and Morocco – and its European implications – and the fact that Rabat has resorted to economic retaliation (by excluding Spain from Operation Crossing the Strait) does not help convince those who doubt the strategy’s convenience or applicability. On the other hand, it should be noted that the effects of the bilateral crisis of 2021 have not affected industrial relations between the two shores of the Strait, showing that the “colchón de intereses” remains operational.

In this situation, three options emerge: 1) give up, assuming that the Maghreb has already missed the nearshoring opportunity and that – if it happens – areas like eastern Europe, Turkey and Egypt are better placed to take advantage; 2) keep trying, but focusing on Tunisia and Algeria in order to reduce the risk of any efforts being undermined by bilateral tensions; 3) keep Morocco as a priority, but without forgetting the other two countries and seeking to create a dynamic of regional cooperation in terms of economic recovery, reindustrialisation and connectivity.

Nearshoring is a medium- to long-term strategy. It should not, therefore, be conditioned by tensions that will sooner or later end up being redirected, but should be based on structural factors like geographical proximity. Keeping Morocco as a potential partner for Spain in this field gives weight to the idea that cooperation can and should be maintained on issues of mutual interest even when differences exist elsewhere. It would also be a way of demonstrating Spain’s desire to help improve relations between Morocco and the European Union. Fundamentally, it would be a commitment based not on appeasement or transactional cooperation, but on taking advantage of a shared opportunity.

Why widen the focus rather than focussing solely on Morocco? As the ultimate goal of nearshoringis to diversify supply, the more countries benefit from it, the better. So, while industrial relations are less developed with Algeria and Tunisia, the potential is there. Of the three options presented, the third – continuing to prioritise Morocco, but working to include Tunisia and Algeria – therefore seems the most reasonable. Let us consider what action is needed to achieve this goal.

The To Do List

Conceptually, nearshoringaligns with the interests and strategic priorities of Spanish policy towards the Maghreb and sounds promising as an idea. The Maghreb countries are certainly candidates to benefit from it, but opportunities can be missed. To prevent this from happening, action must be taken at various levels.

In Spain:

- So far, the discussion around nearshoring has mainly been limited to government circles and think tanks. Economic agents must play a more active role. After all, companies will make their own decisions about whether to invest or not, and in which countries they want to do so.

- At governmental level, infrastructure investment could be increased to structure and connect Spanish ports (especially Algeciras, Valencia and Barcelona, but also Alicante, Tarragona, Cartagena and Málaga) with North Africa and European freight transport networks.

- Explore the possibility of geographical or sectoral specialisation. Investments in the Campo de Gibraltar, for example, could be aimed at strengthening the existing industrial cooperation on both sides of the Strait. Specific strategies can be devised for key Spanish sectors like the automotive and pharmaceutical industries. Tunisia could be a suitable partner in those domains.

- Reinforce cooperation with Morocco at all levels, seeking to overcome the bilateral crisis and strengthening the Europeanisation processes.

In Europe:

- As far as possible, incorporate the EU's neighbours into economic recovery, reindustrialisation and connectivity strategies.

- Insist on the need for technical harmonisation to reduce non-tariff barriers. The negotiations over the Deep and Comprehensive Free Trade Areas (DCFTA) have faced stiff resistance. But without this harmonisation the potential attractiveness to investors is reduced. Careful thought will need to be given to the reasons for such reluctance and whether the mechanisms exist to assuage it.

- Design pilot projects that lead the way and dispel private investors’ doubts. Industrial cooperation across the strait could provide a good example. Show that it is a positive-sum game and that compensation mechanisms exist for those potentially left behind.

- Integrate the Maghreb into the EU’s new African commitment. Bi-continental cooperation can open up new opportunities and above all generate a positive cooperation dynamic in which the Maghreb is the nexus.

In the Maghreb:

- Although Spain and the EU view the Maghreb countries as potential partners in this strategy of reindustrialisation and resizing supply chains, it is the governments and business sectors in Morocco, Algeria and Tunisia themselves that must decide whether this strategy convinces them and what they can do to make it happen.

- To take advantage of this opportunity, administrative and legal reforms are needed without which it will be very difficult to attract private investment. This is all the more pressing given that other candidates in the European neighbourhood (Turkey, Egypt, eastern Europe) are awaiting this investment with open arms.

- The human capital eroded by the COVID-19 pandemic must be strengthened. Human capital is a decisive factor for foreign companies considering relocating their production.

- As far as possible, economic cooperation should be decoupled from political tensions between Maghreb countries and between them and their European partners. Any progress on regional cooperation will increase the attractiveness of the Maghreb countries to potential investors.

In conclusion, Spain can and must promote the idea of nearshoring in the Maghreb, but it cannot do it alone. It will have to accept that the strategy will only gain enough traction if it is accompanied by European support and resources. Equally, the governments and productive apparatus in the Maghreb countries must adopt a more open attitude and make the reforms and investments that enable them to take advantage of the opportunity.

Updated: June 30th 2021

E-ISSN: 2013-4428