Bahrain’s Economy: Oil Prices, Economic Diversification, Saudi Support, and Political Uncertainties

In 2011 Saudi Arabia and the UAE sent troops to Bahrain after unrest in the country. This marked the beginning of a more assertive foreign policy in the MENA region that later culminated in an ill-fated military intervention in Yemen and a boycott of Qatar. Bahrain is a crucial ally and client state of Saudi Arabia, which fears growing influence of Iran among the Shiite majority population of the country. Bahrain’s economic stability is important for its political stability. It is closely connected to oil prices, Saudi transfers, diversification efforts and economic reform.

Low oil prices since the second half of 2014 and domestic and regional political risks have impacted the credit risk and liquidity situation of Bahrain. Bahrain has undertaken considerable economic diversification measures in manufacturing, refining, tourism, trade, and finance. Dependence on oil has been declining since the 2000s, yet oil revenues still constitute a three quarters of government revenues

As a result Bahrain has developed current account deficits in recent years, its fiscal deficit has been rising, and its foreign reserves have been shrinking. International rating agencies lowered their ratings in 2016 and 2017. Support by Saudi Arabia is crucial in the form of oil deliveries of the joint Abu Saafa field and financial transfers, most notably via the GCC development fund that was launched in 2011. Together with Kuwait and UAE it has allocated 7.5 billion US$ to Bahrain.

Macroeconomic Indicators

Bahrain’s oil and gas sector still plays a very important role in its economy with about 19% of its GDP (see Figure 1). This ratio has fallen from 43.6% in 2000 despite the absolute growth in hydrocarbons production, signaling considerable diversification into sectors such as finance, manufacturing, and services. However, oil and gas revenues still accounted for 75,7% of government revenues in 2016 and exports of refined petroleum products (29%) and crude oil (17%) accounted for almost half of total exports. It also needs to be kept in mind that manufacturing industries of Bahrain, such as Aluminum Bahrain (ALBA) and the Sitra refinery rely on oil and gas as important feedstock inputs. ALBA’s exports accounted for 11.5% of Bahrain’s total exports and 30.1% of its total non-oil exports in 2015 and it consumed over a quarter of the country’s unassociated natural gas production.

With initiatives like the free trade agreement with the US in 2006 Bahrain has sought to integrate better with global markets and beyond the oil sector. Yet its trade remains heavily dominated by regional partners. GCC countries accounted for 61.7% of its total non-oil exports in 2016 and Saudi Arabia alone for 33.7%.

The still pronounced dependency on oil showed in macroeconomic data when oil prices slumped during the second half of 2014. Government budget break-even prices of $121 per barrel in 2015 and $132 per barrel in 2016 were way above oil prices that mostly hovered between $40 and $50 during that period. Bahrain started to develop current account deficits, its government debt to GDP ratio shot up from less than 20% in 2008 to almost 100% a decade later. Its foreign currency reserves declined from $6 billion to 2 billion over the last four years and S&P expects its fiscal deficits to hover around 7.5% of GDP until 2020.

Bahrain’s GDP in current prices declined in 2015, although it still increased in real terms. Oil revenues fell steeply from $7.1 billion in 2014 to $4.2 billion in 2015, but government spending was maintained, especially public sector salaries and social welfare transfers that are crucial for political legitimacy in the country, which suffered in the wake of political unrest in 2011. Growing total external debt and foreign FDI inflows were crucial in covering fiscal and current account deficits. Financing such deficits has become essential for Bahrain and has affected the structure of its debts and assets.

Bahrain’s Credit Risk and Funding Structure

Bahrain’s rising public debt is roughly half domestic and half external. By the end of 2016, Bahraini banks held about 83% of domestic public debt. The external debt was mostly held in the form of international conventional bonds, Islamic debt instruments only played a minor role. GCC development funds such as the Arab Fund for Social and Economic Development (AFSED), the Kuwait Fund, the Qatar Fund, or the Islamic Development Bank accounted for $398.3 million of the $12.8 billion outstanding foreign liabilities in August 2017.

The loan to deposit ratio, the ratio of nonperforming loans to gross loans, and the ratio of liquid assets to total assets remained broadly stable for Bahraini banks over the period. Yet there have been growing concerns about credit risk, given the rising debt levels. Another vulnerability is the US dollar peg of the Bahraini Dinar, which has been officially pegged at 0.376 BD to the dollar since 2001 after having been already informally pegged at the same rate since 1980. Should Bahrain not be able to maintain the peg in the future this would result in significantly reduced ability to serve its dollar denominated debt. Slightly more than half of government debt is external and entails considerable exchange rate risks.

Compared to Saudi Arabia, Kuwait, Abu Dhabi, and Qatar, Bahrain has limited oil production and has not accumulated large foreign assets in Sovereign Wealth Funds (SWFs) as these countries have done. It has, however, its holdings in domestic companies, which it administers via the oil conglomerate Nogaholding and the domestic SWF Mumtalakat. Both were established by Royal Decree in 2007. Nogaholding encompasses BAPCO, BAPGAS, Tatweer, and other hydrocarbon related companies. Its dividend payments to the government have been at times interrupted. Mumtalakat’s holdings include ALBA, Gulf Air, and various other companies for industry, tourism, and food processing.

Bahrain also benefits from the GCC Development Fund, which was established in 2011with the goal of financing $20 billion of infrastructure and housing investments in the two oil poor GCC states Bahrain and Oman. This was well before the oil price correction in 2014 and points to structural issues of oil dependency, regardless of oil price levels. The initial plan was to raise $10 billion for Bahrain from the four revenue rich GCC countries Saudi Arabia, UAE, Kuwait, and Qatar. In reality only the former three have contributed and it is unlikely that Qatar will contribute its $2.5 billion, given the current blockade against it by Saudi Arabia, Bahrain, UAE, Egypt, and Yemen. The remaining three GCC donors’ commitments amounted to $7.5 billion by 2017. Of these $6.6 billion were allocated to projects, $3.3 billion of contracts were awarded and $1.2 billion were actually paid from the GCC Development Fund.

Access to international financial markets has become more important for Bahrain since 2014 in order to finance its fiscal deficit. However, at the same time this access has become more difficult and expensive as result of a number of rating downgrades since 2013 (see Table 1). Bahrain was still investment grade with a triple B rating in 2013 and 2014, but it is now rated two notches lower at single B by S&P and Moody’s. It is therefore in junk bond territory. However, S&P has given Bahrain a “stable” outlook in its recent downgrade to B+ because it expects financial support from neighboring sovereigns, most notably Saudi Arabia and the UAE.

Thus the following four factors are crucial for Bahrain’s liquidity situation:

a) maintenance and modernization of the crucial hydrocarbon sector in a low oil price environment

b) economic diversification into non-hydrocarbon sectors

c) Raising new raising non-hydrocarbon revenue streams such as taxes and fees and cutting expenditures, such as subsidies

d) Outside support, mainly by Saudi Arabia and the UAE

Bahrain’s Hydrocarbon and Refining Sector

Bahrain was the first country on the Arabian side of the Persian Gulf where oil was discovered and a refinery was set up. The Bahrain Petroleum Company (BAPCO) struck oil in 1932 and the Sitra refinery started with a capacity of 10k bpd in 1936. Oil also came with increased geopolitical importance: The British Royal Navy moved its entire Middle East command from Iranian Busher to Bahrain in 1935. Oil superseded traditional economic activities such as trade and date farming as the mainstay of the economy. The share of the oil sector in GDP today is at 19 percent, but was still at 43,6% as recent as 2000 (see Figure 1).

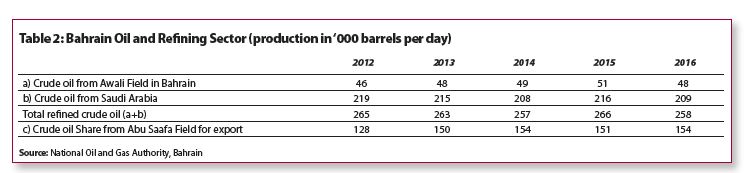

Bahrain’s oil sector can be divided into two parts: On the one hand Bahrain is a refining hub. It is in the process of modernizing its Sitra refinery for which it uses imported crude oil from Saudi Arabia and complements it with production from its onshore Awali field. On the other hand it produces crude oil for export from its 50% share of the offshore field Abu Saafa, which it shares with Saudi Arabia (see Table 2). In terms of revenue the oil exports from Abu Saafa are much more important than the refining margins from Sitra.

In 1958 Bahrain and Saudi Arabia signed a maritime border agreement that gives oil rights to Saudi Arabia in exchange for a share of oil revenues to Bahrain. Abu Saafa was discovered in 1962 and production started in 1966. In 1972 Bahrain and Saudi Arabia agreed on a sharing agreement that gives 50% of the revenues to Bahrain without charging it production costs. Historically Bahrain has received significantly more than its 50% entitlement. Between 1996 and 2004 Saudi Arabia actually allotted 100% of the revenue to Bahrain and in 1986 it continued payments, although the Al Saafa field was mothballed because of low oil prices. Rather than a joint venture, Al Saafa is a flexible Saudi subsidy scheme for Bahrain. Tellingly, Saudi state owned oil company Aramco operates the field on behalf of both countries. The Saudi largesse for strategic reasons makes the field even more important for Bahrain and underlines once more the importance of support from Saudi Arabia for the economy of the country.

The refinery at Sitra is the second most important aspect of the Bahraini hydrocarbon complex. It imports most of its crude oil feedstock from Saudi Arabia and tops it up with domestic production from its Awali onshore field. This field has peaked decades ago at around 70k bpd and production fell as low as 20k bpd. With an ambitious revamping program that included drilling of new wells and enhanced oil recovery Bahrain brought production levels up to around 50k bpd. In 2009 it launched the Nogaholding subsidiary Tatweer for this purpose that invested $3.43 billion between 2009 and 2015. Bahrain plans to increase its oil production steadily over the next 20 years, but it remains to be seen how realistic and sustainable domestic oil production levels will be. Bahraini oil reserves are limited at currently 633 million barrels, which roughly equals a reserves to production ratio of 34 years.

In 2010, the government of Bahrain announced the BAPCO Modernization Program, which will be the single largest investment the company has ever undertaken. It will increase the refining capacity at the Sitra oil refinery by a third, will improve its product mix, and reduce the sulphur content of the oil produced. The Sitra expansion will cost $5.7 billion and is slated for completion by 2021. It is also building a new pipeline from Saudi Arabia that will have a capacity of 400k bpd and will replace the existing pipeline that was built in 1945 and only has a capacity of 235k bpd.

Another pillar of Bahrain’s hydrocarbon economy is its domestic production of natural gas, much of which is unassociated gas from the Khuff gas reservoir. Natural gas production has increased slightly over the last five years. It is crucial for domestic consumption and industrial ventures. Like other Gulf countries Bahrain has a skyrocketing domestic energy consumption and a natural gas shortage. Of the Khuff gas 43% is being sold to the Electricity Directorate, 26% to ALBA, 10% to BAPCO, and 9% to Gulf Petrochemicals Industry Company (GPIC). Natural gas is also used for oil field injection to maintain pressure in mature reservoirs.

Bahrain is also building an import facility for Liquefied Natural Gas (LNG) to complement its energy mix. The UAE has already built such an LNG terminal in Fujairah. The Bahrain LNG terminal is expected to be completed by 2019. Most likely LNG import prices will be above the current price level for domestic natural gas and might affect profitability of industrial end users such as ALBA or GPIC.

Economic Diversification: Finance, Services, Tourism, Trade

Since the late 1960s Bahrain has sought to diversify its economy towards non-oil sectors such as finance, services, logistics, tourism, and industry. In October 2008, the Bahraini government reiterated such diversification strategies in its long-term planning document “Vision 2030”.

Finance

The financial sector in Bahrain received a supporting impetus with the outbreak of civil war in Lebanon, which used to be the financial center of the Middle East until then. Many banks and financial service providers moved to Bahrain in the process, which was able to establish itself as a new financial hub within the Gulf and the wider MENA region. In 2016, the financial services sector was the single largest non-oil contributor to the Bahraini economy, accounting for 16.5% of real GDP. Bahrain has the largest concentration of Islamic finance institutions in the GCC region, including Islamic banks, Takaful and Retakaful firms. Bahrain hosts the industry’s global oversight body, the Accounting and Auditing Organisation for Islamic Institutions, as well as the Islamic Rating Agency and the International Islamic Financial Market. In 2017 Islamic banks’ assets accounted for 14.8% of total banking assets.

There is some debate whether finance should be regarded as an end of diversification or rather just a means. Considerable proliferation of financial centers has taken place in other cities of the Gulf, such as Dubai, Doha, Abu Dhabi, and Riyadh. Hence Bahrain has lost some of its uniqueness and first mover advantage and there is a certain risk of regional oversupply. Some financial instability has also occurred in the wake of the global financial crisis and the Dubai real estate bubble. Bahrain’s Arcapita Bank filed for Chapter 11 bankruptcy protection in 2012. In 2017 the central bank of Bahrain (CBB) was Arcapita Bank’s largest creditor, holding approximately $232.5 million of the bank’s debt.

Manufacturing and Construction

Aluminum Bahrain (ALBA) is the crown jewel of the Bahrain manufacturing sector. It has a capacity of 936k tons per year, which makes it the fourth largest aluminum plant globally by individual smelter capacity. With an investment of over $3 billion it plans to add a sixth potline in 2019, which would add approximately 540k tons to ALBAS’s existing capacity. It contributes 30.1% to Bahrain’s non-oil exports and 11.5% of its total exports. 69.4% of its capital is being held by the SWF Mumtalakat and a minority share of 20.6% by Saudi Basic Industries Corporation (SABIC). ALBA was founded in 1968 and was a pioneer of heavy industries in the Gulf. It marked the beginning of diversification strategies that capitalized on the availability of cheap energy feedstock in the region. This relative advantage tends to erode, as with the exception of Qatar countries in the region have to increasingly rely on LNG imports and reconsider their very low administratively set natural gas prices. ALBA has entered into an agreement with Nogaholding over prices for its natural gas for the period 2015-2021. From $2 per mmbtu they have been raised by $0.25 per mmbtu each year and will reach $4.00 per mmbtu by April 2021.

In contrast to Dubai Aluminum, ALBA has sought to expand into aluminum processing early on in an effort to enhance the value chain of its aluminum production. Bahrain also has industries for steel and food processing and has sought to use its privileged market access to the US via its FTA as a means to attract Asian textile producers who could use Bahrain for upgrading production steps and as a springboard to the US market.

Construction is an important sector of the economy with a 7% GDP share (see Figure 1). Affordable housing for broader segments of the population will need to expand beside the ubiquitous luxury real estate projects that are common in the Gulf. It is an important priority for the government, also for reasons of political legitimacy.

Services, Logistics, Trade and Tourism

Bahrain is an old trading hub in the Gulf and has sought to leverage this position in regional trade. However, like in finance it has been superseded by Dubai, whose Jebel Ali port is also an important port of call for the US navy, although it does not officially figure as a base like Bahrain, which hosts the US 5th fleet.

Another major non-oil sector in Bahrain is tourism. Nearby Saudi Arabia is connected with the island via a causeway and many Saudi citizens visit Bahrain to escape the moral and cultural strictures of their country. Alcohol is legal in Bahrain and it has a diversified offering of beach resorts and nightlife. In 2016, 12.2 million visitors crossed the causeway to enter Bahrain. Bahrain and Saudi Arabia have agreed to build a second bridge, with both road and railway links.

Bahrain again was a pioneer in the region when it attracted the first Formula 1 race in the region in 2004. Abu Dhabi followed suit with its own Formula 1 race event in 2009. Because of limited hotel facilities, a considerable part of the hotel business around Bahrain’s Formula 1 race occurs in Dubai with visitors only flying in and out for the event. In 2011 the event had to be cancelled because of the political unrest in the country, marking considerable vulnerability.

Bahrain’s airline Gulf Air has lost out in the competition with other Gulf airlines such as Emirates in Dubai, Qatar Airways or Etihad in Abu Dhabi and has developed into a financial burden for the government. Mumtalakat owns 100% of Gulf Air, which has undergone a five-year restructuring plan since 2012. Government support payments could be reduced over time, but will reach a cumulative $1,423 million by 2018.

Reform Measures: Subsidies, Fees, Taxes, Human Resources

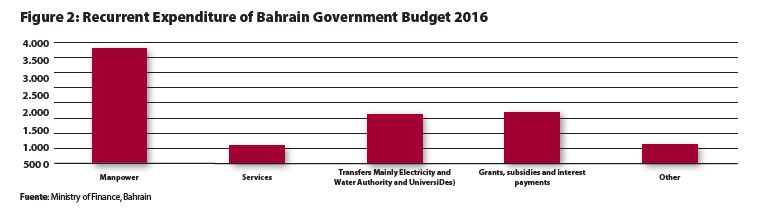

Recurrent expenditure is the lion’s share in Bahrain’s government expenditure. With a cumulative $8,023 million in 2016 it was much larger than project expenditure, which amounted to $1,092.8 million. The lion’s share of recurrent expenditure in turn is manpower with a share of 45.8% in 2016. This demonstrates that employment of Bahraini nationals is still largely concentrated in the public sector. Salary cuts would be politically sensitive, but the government eyes reductions of bonuses and non-core allowances of up to 75%. Above all, reform measures have focused on cutting subsidies or redirecting them towards lower income segments of the population and raising taxes and fees.

The Bahraini government has announced plans to introduce a value added tax from 2018, with a grace period up to 2019. It has also raised unified gas prices by $0.25 per year, which will continue until 2021. The total value of savings from cutting subsidies and raising fees are expected to yield an annual saving of approximately $1.5 billion per year, which is equivalent to 4.4% of GDP and more than a third of the fiscal deficit of 2016. However, some of the measures may also increase inflation and could reduce competitiveness of some enterprises.

With the Tamkeen training program the government seeks to improve education and qualification of young people in order to prepare them for a better entry into the labor market. The level of unemployment among Bahraini nationals hovers around 4%. Of a population of roughly 1.5 million only 46% are Bahraini nationals. The share of expatriates in the labor force is close to 80% and even higher than in the overall population.

Political Risks, Intra-Gulf Transfers, and Bahrain’s Strategic Importance for Saudi Arabia

Financial support for Bahrain by Saudi Arabia and to a lesser extent the UAE and Kuwait is crucial for Bahrain’s liquidity situation. It is implicitly assumed by rating agencies in their assessments of the country. Support comes in the form of investments of the GCC Development Fund, loans by Gulf development funds and above all Bahrain’s production share in the Al Shaafa field, which has often been above the agreed 50%. Saudi Arabia and the UAE also lent their military support when they sent troops to Bahrain in the wake of domestic unrest in 2011.

Bahrain’s strategic importance for Saudi Arabia derives from its geographical location, i.e. its close vicinity to critical Saudi oil installations, which are sometimes as close as 40 kilometers, for example Saudi oil fields (Ghawar, Abqaiq, Abu Safah, Qatif, and Berri), the oil export terminals (Ras Tanura, Al Juaymah), the oil processing facilities at Abqaiq, and the equally critical water treatment facilities of Qurayyah which is indispensable for water injection at many fields such as Ghawar, Abqaiq, Berri, and Khurais.

Under no circumstances Saudi Arabia could accept Iranian influence in Bahrain. It perceives such a threat, because Iran has made historical claims to the archipelago in the past and Bahrain has a Sunni ruling monarchy, but a majority Shiite population with ca. 60%. The Iranian threat perception in Saudi Arabia and other Gulf countries is overwhelming. It informs much of Saudi Arabia’s regional foreign policies, ranging from its support of Sunni insurgents in the Syrian civil war, its initial protest against the Iranian nuclear deal (the “Joint Comprehensive Plan of Action”/ JCPA), its war in Yemen (since 2015) in which it has become bogged down, and the inconclusive blockade of Qatar since 2017.

Bahrain has been ruled since 1783 by the Sunni al-Khalifa family, a clan from the Atabi tribe that is originally from Qatar. The Khalifa seized the trading entrepot from Persia at that time. When the British decided to get out of the Gulf at the end of the 1960s, both Saudi Arabia and Iran made claims to the island, with Iran asserting rights emerging from its pre 1783 rule. In the end the United Nations denied the Iranian claim and argued in favor of formal independence of Bahrain, which followed in 1971.

Since then Iran has accepted Bahraini sovereignty, but lower ranking Iranian officials have made occasional remarks from the second row about renewed claims of Iranian sovereignty that have disturbed politicians from Bahrain and other Gulf countries. Such remarks are all the more disconcerting for them as domestic conflict in Bahrain has increasingly taken sectarian undertones with the Shiite majority population rebelling against the Sunni ruling monarchy and complaining about limited political participation and economic discrimination. Shiites are for example heavily underrepresented in the military, the police and the security services, which are staffed by Sunnis, sometimes of foreign origin like the large number of Pakistanis in the police forces.

The real influence of Iran is arguably less than perceived by Saudi Arabia and other Gulf countries. Ties between the Shi'a in Bahrain and those in Iraq are much stronger than those with Iran according to US cables that were published by WikiLeaks, yet perceptions matter. Meanwhile the political and sectarian conflict in Bahrain has been increasingly tense since the unrest in 2011. On 17 July 2016, Bahrain’s High Civil Court dissolved the Shiite Al Wefaq National Islamic Society. In May 2017, the police in Bahrain arrested 286 people and killed five in Diraz as part of an operation to arrest militants, leading to legal proceedings against 60 persons for forming a terrorist organization and using weapons and explosives.

Bahrain is a strategic priority for Saudi Arabia also because of its own large Shiite minority that is concentrated in its oil rich Eastern province. Saudi Arabia is afraid that Iran could gain influence over this Shi’a population or that unrest in Bahrain could spill over to its Eastern province. For all intents and purposes Bahrain can be regarded as a Saudi client state with only limited freedom to maneuver when it comes to regional foreign policy issues. Beside Saudi Arabia and the UAE it was the only GCC country that participated in the blockade against Qatar with Oman and Kuwait abstaining. Apart from its alliance with Saudi Arabia, Bahrain has also close relationships with the US whose fifth fleet it is hosting in Manama. In 2002, the U.S. designated Bahrain a “major non-NATO ally”.

Against this backdrop the willingness of Saudi Arabia to assist Bahrain financially must be regarded as very high. Its ability to pay should still be intact over the next few years, but it is eroding as it repatriates foreign assets to cover its own fiscal deficit. Its foreign reserves have decreased from $737 billion in August 2014 to $486 billion in November 2017. Transfer payments are likely more sustainable and less transactional than in the case of Saudi payments to Egypt. Still, Saudi Arabia and the UAE might ask for increased equity participations in the Bahraini economy in return for any increase in financial aids. Especially the UAE has pushed for such arrangements in the case of Egypt.

Keywords: Bahrain’s Economy; MENA Region; Oil Prices; Political Uncertainties; Saudi Arabia; Economic Diversification

E-ISSN: 2013-4428

D.L.: B-8439-2012